By Brittany Leona Parks, Writer, my529, Utah’s Education Savings Plan

March 5, 2024

Educating children early and often about financial concepts develops saving habits for their first major purchases—a car, higher education, and future housing expenses. One of the best ways for children of all ages to save is to become a mindful consumer.

When children are young, you can invite them to hold the grocery shopping list and categorize which items are wants versus needs. Discuss ads to help them discover what they should prioritize from among the bombardment of suggestions. Finally, have them rank their wish lists to identify comparable value among their items and avoid impulse purchases.

Once children begin earning money, work with them to make a budget and consider what they hope to buy over the next few months and years. They may see that saving for one item may require postponing another. Note these competing purchases and help them organize their list into short-term and long-term goals. This approach demonstrates that saving for important, expensive items starts with small amounts over time, alongside their other short-term savings goals.

To support achieving their long-term goals, encourage them to make small regular deposits in a 529 account. “A low- and moderate-income child with school savings of $1 to $499 … is about four times more likely to graduate from college.”* They may be more likely to accomplish their career goals if they have already financially invested in them, whether college, technical college, or Registered Apprenticeships.

As they approach high school graduation, they could also begin to invest in an emergency fund for unanticipated future needs. A car repair or job loss could cost them in credit card interest if they haven’t designated savings for life’s many unknowns.

Equipping and nurturing the young people in your life with saving habits will allow them to strengthen their financial skills now to focus on achieving their short-term and long-term goals later.

my529 is Utah’s official and only 529 education savings plan and has been helping families save for college for over 25 years. Learn more at my529.org.

*Elliott, William. (2014). Assets and Education Initiative. 2013. Building Expectations, Delivering Results: Asset-Based Financial Aid and the Future of Higher Education. Biannual Report on the Assets and Education Field, July.

About the Author

Brittany Leona Parks is a writer for my529, Utah’s educational savings plan. When not researching financial best practices for children, she is trying these strategies out on her own two kids, hiking with her family, and participating in entirely too many book clubs. She previously spent 8 years marketing to the financial and legal sectors.

By Mary Morris, Virginia529 CEO and College Savings Plans Network, Chair

As we step into 2024, let’s take a moment to reflect on the progress made in education savings over the past year. In 2023, 529 plans across the nation seemed to shake off some of the post-pandemic doldrums of the prior year and saw significant growth, with more families than ever investing in their loved one’s future education.

According to recent data, the amount invested in 529 plans increased by 14% compared to the previous year, to $470 billion in total savings — closing in on half a trillion dollars in education savings!

Particularly encouraging is that the number of 529 accounts opened nationwide reached an all-time high in 2023, surpassing 16.4 million. Account growth can better indicate the impact of 529 plans as it is based on the people committing to investing in the future, whereas the financial markets impact asset growth. 529 plans across the country are dedicated to encouraging people of all household income levels to open 529 accounts and finding ways to increase awareness of the programs and provide affordable options.

Another indicator of success in 529 plans is average account size growth — in 2023, that increased by 11%. The national average account size now approaches $29,000, covering more than two years of tuition at a typical public, in-state college or university — and going even further for a student opting to start at a community college. These figures highlight the positive impact of consistent saving and careful planning. They also show more work to do as the average student loan debt held by borrowers now tops $37,000.

So, for 2024, what are some simple ways to approach education savings that will really work? Here are seven practical tips to help you succeed in education saving:

- Get started: Begin your savings journey today. Most 529 programs have low opening balance requirements — as little as $5 or $10 (and, in some cases, no contribution) may be required to open a 529 account.

- Use “found” money: Take advantage of unexpected windfalls, such as tax refunds, by putting them into your 529 account. This will boost your savings and maximize your long-term growth potential. Many 529 programs make this contribution easy by providing a direct deposit option when filing your taxes.

- Make saving easy: Set up automatic contributions from your bank account or paycheck to ensure consistent saving without having to think about it. Just $5 or $10 a month consistently going to your 529 account will make a real difference in the future.

- Share your goals and encourage gifts: Let your student know about their 529 account and encourage contributions from family and friends for special occasions. Gifting platforms and options abound today, making it easy to jumpstart educational savings — with safe and secure ways to use social media and other messaging to encourage gift contributions.

- Increase contributions gradually: Once you take Step 1 and get started, try to increase your contribution rate at least annually, target a percentage increase per year, or take action when you get that raise at work, child care costs decrease, or you pay off that student loan you carried because you didn’t have a 529 account.

- Communicate with your 529 plan: Log into your account frequently, review and update your account details at least annually, and ensure that everything is accurate and aligned with your goals— the start of a new year is a great time to check in if you didn’t do it at year-end.

- Review your investment strategy: Check your portfolio allocation at least annually to ensure it matches your savings goals and risk tolerance.

By following these tips and staying committed to your education savings goals, you can set yourself up for success in 2024 and beyond. With careful planning and consistent effort, you can provide valuable opportunities for your loved ones’ — or your own — future education.

About the author: Mary Morris is the CEO of Virginia529 and the chair of the College Savings Plans Network.

By Steve Jobe, Senior Vice President, Vestwell

February 20, 2024

Anyone who’s been or has sent a child to college knows firsthand how expensive obtaining a degree can be and how quickly that cost has risen. Just how big a problem is this? How can we address the damage already done? Who can help Americans avoid the burden in the future?

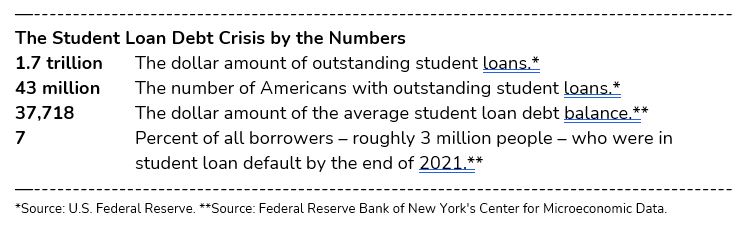

The amount of student loan debt is staggering. And, the number of Americans affected is significant – over 15% of adults in this country. Student loan debt is both a burden for American families and a drag on the country’s economy. Perhaps you’ve experienced this firsthand – did you put off contributing to your 401(k) because you had too many student loan payments left? According to Vestwell’s annual “Saving Trends Report, 93% of survey respondents with student loans reported that their student debt had affected their ability to save. Other common delays include moving out of the parents’ house, or buying a new car or a first home.

Employers to the rescue. Thankfully, there are workplace solutions to help employees repay their student loans. Employers have begun using services such as Gradifi, a benefit service that gives employers a simple, streamlined way to provide a match to employees who are still repaying their student loans.

Of course, the best way to reduce student loan debt is to incur little or none in the first place. So what can the average American do to best prepare for this future cost? Take advantage of the two things everyone has at their disposal: time and the tax benefits of a 529 plan.

One boost to incorporating 529s in the workplace has come from several states that provide tax credits to incentivize employers to promote savings in a 529 plan. Currently, Arkansas, Colorado, Idaho, Illinois, Nebraska, Nevada, and Wisconsin offer tax benefits to employers who match their employees’ contributions to a 529 plan. Along with this financial wellness strategy, many employers already make it easy to contribute to a 529 plan by allowing employees to make a contribution through the payroll process. These types of incentives are helping to spread the word about the benefits of saving for future education expenses instead of relying on student loans.

Why 529 Plans? As those who frequent this blog know, 529 plans are tax-advantaged savings plans to help offset the cost of higher education. They can be opened by anyone and assigned to any beneficiary – a child, a grandchild, a niece or nephew, a friend – even yourself or your spouse. 529 plans are sponsored by states, so their rules – such as tax incentives – differ from state to state. However, in all cases, the money grows on a tax-deferred basis. As long as it’s used for “qualified” education expenses, future withdrawals aren’t subject to either state or federal taxes. They can even be rolled into a Roth IRA now if eligible balances remain in the account.

However, according to the same survey, only 42% of savers are at least somewhat aware of the tax benefits of 529 Plans, and less than 5% of those surveyed with a Vestwell-managed 401(k) currently have one. So, while the benefits of starting a 529 plan are numerous, too many Americans need to be made aware of them, and fewer take advantage.

A 529 plan might be an effective way for you to help someone you love reduce reliance on future loans, and with many employers beginning to offer them as a part of their benefits and financial wellness offering, they can be set up easily to prepare for future educational expenses. Check with your benefits provider or HR department to ensure you are fully aware of all financial wellness benefits you may be eligible for. Open an account and start saving as soon as possible; regardless of how much you contribute, every dollar saved reduces the amount of student loan debt in the future.

About the Author

Steve Jobe is a Senior Vice President at Vestwell, where he oversees strategy and relationship management of the firm’s 529 and ABLE programs. Steve also serves on the College Savings Foundation’s Board and the Municipal Securities Rulemaking Board (MSRB)’s Municipal Fund Securities Advisory Group.

By Roby Smith, Iowa State Treasurer

February 13, 2024

Ahhhh, love! Nat King Cole had it right: “‘L’ is for the way you look at me …” And looking at the benefits of 529 plans, there’s a lot to love!

L: With LIMITLESS possibilities of what path your child may choose for their future, a 529 account can help turn their dreams into reality. Today’s children are preparing for careers that are the backbone of society, and jobs we haven’t even imagined yet! To help prepare them for wherever their journey may lead, your 529 funds can be used at any eligible educational institution in the United States, both in-state and out-of-state, and abroad.

O: Investment OPTIONS allow each Participant to investaccording to their own risk tolerance and investment strategy. With a diverse selection of investment options, 529s can help keep your family’s education savings goals on track.

V: It takes a VILLAGE! With the rising cost of education, parents don’t have to save alone. Invite friends and relatives to contribute to your child’s account. Holidays, birthdays, and other special occasions are the perfect opportunities to let others know just how easy it is to contribute. Every dollar saved matters by reducing the burden of borrowing and the amount of debt your scholar may have.

E: EXPENSES beyond just tuition at two- and four-year education institutions are qualified withdrawals; use account funds for room & board, books, supplies, fees and equipment, including a computer. While apprenticeships don’t typically involve a tuition bill, there can be fees, books, supplies, and other required equipment.

Love’s transformative power shows the children in our lives how important they are to us and enables them to know we believe in their potential. Investing in their future with dedicated education savings is an easy choice with the L-O-V-E benefits of 529 plans.

About the Author

Iowa State Treasurer Roby Smith is the administrator of Iowa’s 529 Education Savings Programs, College Savings Iowa and the IAdvisor 529 Plan, with over $6.4 billion invested and more than $5.2 billion in qualified withdrawals.

Why 529 college savings plans are perfect for technical and vocational pathways

By Jackie Ferrado, Associate Director for Community Engagement, Washington 529 College and Education Savings Plans (WA529)

February 6, 2024

The landscape of higher education is constantly evolving. It has even more so in the past few years as students have suddenly begun learning, studying, and networking from behind the screen. Recognizing that learning can happen from anywhere, at any time, and in a variety of ways is the foundation for increasing access to higher education.

Diversity in education

When we think of higher education from a holistic point of view, it’s important to consider that employees who come to the workplace with education and training from vocational, technical, and apprenticeship programs are equipped with practical knowledge and skills that allow them to be job-ready and prepared to meet the demands of the specific industry. Through practice and hands-on learning alongside licensed professionals, apprentices gain insights into the real work that may not resonate as well from a classroom setting alone. This approach can be meaningful to employees and employers alike.

Supporting economic recovery

The cost of pursuing a degree continues to increase, and students may find themselves taking out more student loans than necessary and receiving a credential that may or may not best meet their career goals. Through individual savings efforts and a careful and thoughtful educational path that supports career goals and passions, students with technical and vocational training can often gain valuable skills at a more affordable cost and enter the workforce sooner. As a result, these students may find themselves in a high-demand position with a competitive salary.

Using 529 funds for trade schools and apprenticeship programs

Families who are saving for their child’s future education in a 529 plan can be confident that if their child prefers a program through a technical, vocational, or apprenticeship pathway, their savings will cover a variety of those expenses.

Here are three tips for maximizing the benefits of a 529 plan for technical, vocational, and apprenticeship training programs:

- Research qualified institutions and apprenticeship programs: One of the first things to confirm is that the trade school meets the criteria as an eligible educational institution, or the apprenticeship program is registered with the U.S. Department of Labor. To search for trade schools, technical schools, career training, or certification programs use this career search tool sponsored by the Department of Labor. Having this information confirmed ahead of time will prevent any surprises later.

- Understand qualified educational expenses: 529 savings plans can cover various expenses, such as tuition, fees, required books and supplies, and some room and board expenses. Additionally, apprenticeship program-related materials and equipment may also be qualified. To be sure, the student and parents should review chapter 7 in IRS Publication 970 for specific details.

- Watch for updates or changes: Education policies, regulations, and processes can change over time, and these changes can have both positive and negative impacts. It’s always best to keep up on news and information, particularly that coming from your 529 administrator or a financial or tax advisor.

Whether a student chooses to continue their education and earn a degree or certificate for their training, their options are wide open, and the experience will provide them with a positive and lasting impact.

By embracing these diverse pathways and using savings options like a 529 plan, these future students can pursue careers that satisfy their passions and help them build a fulfilling career.

In the words of Malcolm X, “Education is the passport to the future, for tomorrow belongs to those who prepare for it today”. Let’s give the younger generation the encouragement to pursue their dreams, the tools and information to be financially prepared and the opportunities to create their educational pathways from the variety of available options.

About the author:

Jackie Ferrado serves as the Associate Director for Community Engagement with the Washington 529 College and Education Savings Plans (WA529). Since 1998, tens of thousands of students have used more than $1.7 billion of their WA529 savings to attend colleges and trade schools in the U.S. and at least 15 foreign countries. Outside of work, Jackie enjoys baking, reading, and spending time with her three grandchildren.

After a late release of the 2024-25 FAFSA, students will soon receive their financial aid offers. Here are three steps to help you prepare to pay the bill and set your student up for success.

Step 1 – Find the Net Price and Reduce Costs

The financial aid offer itemizes the aid for which your student qualifies for the entire academic year. Use the financial aid offer to determine the out-of-pocket cost to attend that school, often called the net price. Direct costs billed by the school include tuition, mandatory fees, required equipment and on-campus housing. You can reduce costs by applying for a waiver for things the student might not need, such as health insurance or optional fees.

Step 2 – Amount Owed for the Year and for Each Term

Once you have the net price for the year, calculate the net price for each term. Tip: Don’t include federal work-study since this aid must be earned throughout the year.

Step 3 – Make a Plan to Pay the Bill

Accepted students receive the bill a few weeks before the start of the term. However, now is the time to start planning how you will pay the amount owed to get payments in by the required date. Many families use a piecemeal approach, pulling from various sources, to pay the bill.

Scholarships

Private or outside scholarships are a great way to close the gap. Not all scholarships can be used in the first term. Subtract the scholarship only for the term(s) when funds will be received.

529 Account

Look at your 529 account. Determine how much you want to use for each term in year one and for all subsequent years. A few weeks before the bill is due, schedule your withdrawal request. The servicer needs ample time to get the funds to the school.

529 Withdrawals – Tips for Success:

- Always request your withdrawal during the same tax year that it will be used.

- Add any wire transfer fees to the requested amount if you plan to wire funds.

- Don’t withdraw more than you need. Any withdrawal not used for qualified expenses (as defined by the IRS) may be subject to taxes and/or penalties.

- Coordinate expenses with the American Opportunity Tax Credit or the Lifetime Learning Tax Credit for a tax-free withdrawal. Consult a tax professional for advice or assistance.

Other Savings

If you have savings besides the 529 account, determine the amount you want to dedicate to the bill each term. You’ll also need to plan for indirect expenses such as books, supplies, and incidentals like laundry. Student earnings can be a big help with these expenses.

Payment Plans

Many schools offer payment plans to help manage payments as part of a family’s budget. Most plans are interest-free but may charge a fee.

Student Loans

Families may also consider borrowing a Federal Plus Loan or other private education loans. Tip: Be sure to use full-year amounts when setting up a payment plan or applying for student loans.

For more information about paying for school and other resources, visit the College Savings Plans Network (CSPN) at collegesavings.org.

About the author:

Eva Giles is the College Savings Program Manager for the Finance Authority of Maine, administrator of NextGen 529®. NextGen 529 is Maine’s section 529 plan which many families use to save for higher education. Outside of work, Eva and her family spend time hiking and enjoying the natural beauty Maine has to offer.

By Lael M. Oldmixon, Executive Director, Education Trust of Alaska

As a parent, envisioning your child’s future and education journey is natural. After all, don’t we all have big dreams for our children? Still, the 18-year time horizon leading up to college or post-high school training can feel simultaneously daunting and far enough away that procrastination may derail best intentions. Here are a few building blocks to help keep you on track and pointed toward your end goal.

Start early

Starting early and making regular contributions can simplify and make goals more attainable. College can be expensive, and it’s easy to feel overwhelmed by the amount you’ll need to save. My spouse and I utilized a cost calculator when our children were still in diapers. We realized that getting to our aspirational savings goal would cost the equivalent of an additional monthly mortgage payment (spoiler, that was extra money we didn’t have at the time). At that point, we reassessed the goal. We kept saving what we could, incrementally increasing as our kids graduated from diapers to big kid clothes, trikes to bikes, and little plastic sleds to skis. Soon, our oldest will enter high school. And because we’ve saved incrementally over the past 14 years while benefiting from compounding tax-free interest, the remaining amount we hope to save seems entirely manageable.

Save often

It’s not a new concept, but following the keep-it-simple approach, saving even small amounts systematically over a long period of time can add up in big ways, especially when using a 529 education savings plan. Systematic saving is a strategy where you set up automatic contributions to your 529 plan. This method is also known as “set and forget it.” This way, you won’t have to remember to make monthly contributions and are less likely to spend the money on other expenses. When our kids were little, my husband and I invited family members to support our savings goals by using Bill Pay from their bank for small $25 monthly contributions and gifting tools for birthday or holiday contributions.

Focus on the building blocks

Saving for your child’s college education is an important financial goal that requires careful planning and dedication. And it doesn’t have to be hard:

- Open a 529 education savings plan.

- Take advantage of systematic savings.

- Save what you can now and increase your contributions as you graduate from other expenses like diapers and daycare.

- Keep a long view of your goals.

- Small contributions can make a big difference over time.

- Start saving today, and you’ll be one step closer to achieving your goals.

Be flexible

The last bit of encouragement I’ll leave you with, dear reader, is that life can get in the way of the best-laid plans. So, don’t beat yourself up if you have to pull back on the amount or frequency of your contributions. Celebrate every penny saved and try to stay on course by saving something each month, even if it’s a little bit. It all adds up.

About the author:

Lael M. Oldmixon, M.Ed is the Executive Director of the Education Trust of Alaska, which offers Alaska’s three 529 plans: Alaska 529, the T.Rowe Price College Savings Plan, and the John Hancock Freedom 529. She lives in Alaska with her spouse, two children, and two dogs.

By Rodger O’Connor, Associate Director for Marketing & Communications, Washington State’s College Savings Plans (WA529)

January 16, 2024

It’s January, which means football everywhere you look, on seemingly every channel at all hours of the day. There are college football bowl games, pro football games, football game replays, and even shows discussing nothing but fantasy football. If you’re a fan, it’s glorious.

But even if you’re not a fan, there is still a great reason to watch football: There is so much you can learn about college savings.

Wait, what?

OK, stay with me here. There are dozens of similarities between the game of American football and financing your student’s future education. You might have to squint your eyes and turn your head sideways a little for them to become clear — but I promise, they’re there. Starting with the most basic:

Make a game plan

Before they take the football field, good coaches make a game plan. They study the opposing team and devise a plan to maximize success. This is also important with education savings. Think about how much you want to put away for your student and how much you can afford to set aside each month. But don’t be afraid to change your approach if your student’s plans change. Even the best coaches need to call an audible once in a while.

Mix up your playbook

If a football team ran the same play every time they lined up, their success would be limited. Similarly, your savings strategy shouldn’t be one-dimensional. In addition to setting up monthly contributions, consider ways to boost your savings when opportunities arise. For example, consider socking away a portion of your tax refund or invite family members to make gift contributions for special occasions. You can also diversify your investments. If your state offers both 529 prepaid tuition plans and 529 investment plans, saving with both types can be a great strategy. A prepaid plan provides peace of mind, while the investment plan can potentially reap greater returns. If it looks like your savings plan may fall short of the goal, don’t panic. Many families successfully add to their savings playbook by applying for scholarships, grant aid, and guaranteed student loans to augment their savings.

Don’t depend on the Hail Mary play

Many successful football teams patiently build long scoring drives. Starting your savings plan when your student is young allows you to take your time. Putting away a little at a time for many years is not only easier on the monthly finances, but it also might prevent you from having to throw it deep in the last minute of the game. Begin when they’re young, be patient, and chip away.

Celebrate your win!

When you successfully build and execute a solid education savings game plan, you and your student can both end up enjoying the spoils of victory. Few things in life are sweeter than graduating debt-free! Now get out there and start saving!

About the author

Rodger O’Connor is Associate Director for Marketing & Communications for Washington State’s College Savings Plans (WA529), which includes the GET Prepaid Tuition Program and the DreamAhead College Investment Plan, Since 1998, tens of thousands of students have used more than $1.5 billion of their WA529 savings to attend colleges in all 50 states and at least 15 countries worldwide.

By Jørn Earl Otte, Hartford Funds’ Strategic Marketing Consultant for SMART529 in West Virginia

January 8, 2024

This is the year! You’ve made the commitment – you are going to start setting aside money for your little one’s higher education.

Excellent! Your child or grandchild will be very thankful, and your New Year’s Resolution to start that 529 plan might be one of the easiest resolutions to keep! But where to begin?

The idea of saving for college or trade school can be scary, and the options available can seem overwhelming. With so much in the news about the rising cost of college, it can feel like saving for your child’s future is too big a burden to bear. But you don’t have to feel that way. There are ways to save money for your child or grandchild that can be simple, effective, and stress-relieving.

Here are three simple and effective things you can do to start saving for your child’s future education.

1. Make a monthly “everything” budget: When folks are living paycheck-to-paycheck, the idea of saving even a little bit of money seems too daunting. Groceries, car payments, mortgage, or rent – there appears to be nothing left over. However, if you take a closer look at your monthly expenses, you may be surprised to learn that you have some money left over, but it has been used for things you don’t need. Sit down one evening and write down every single bill you have for the month. Water, electricity, and so forth, but also streaming services, cell phone plans, magazine subscriptions, how many times you ordered dinner-to-go, and how many bags of chips you bought at the grocery store. Everything. Down to the last penny. It may take a little while, but knowing exactly where your money is being spent can be eye-opening. Then, write down your monthly income. Odds are the two figures are pretty close, and likely too tight for your comfort. Look at the list of your monthly expenses – Do you need to spend $100/month on fast food? What about those subscription services? And those magazines? Do you actually read them, or do they collect dust? Be honest with yourself, and you will likely find at least a few dollars each month that can be set aside for something more significant than binge-watching a 1980s sitcom.

2. Open a 529 account: No one knows what the future holds. Your child or grandchild may go to college in-state, or they may fly across the country to follow their dreams. They may love working with their hands and pursue a career in carpentry, or they may get excited about the idea of becoming an electrician. Whatever they may do, you can prepare for it financially with a 529 plan. While most people think 529 plans are just for tuition at traditional four-year colleges, they can be used for so much more – vocational school, technical school, apprenticeships, books, supplies, room and board, and more. And you can feel good knowing that, no matter how little or how much you save for them, every dollar you give them is a dollar they won’t have to borrow from a lender to pay back for the next 20 years. Check out the 529 plan available in your home state, or compare various plans from around the country: www.savingforcollege.com (Read on for more about this).

3. Start small, commit to growth: You will need to check with your own state’s 529 plans to determine what minimums, if any, may exist for opening a plan, and what tax benefits may be available to you. You may also need to seek out the advice of a financial professional to determine which 529 plan is right for you – your own state’s or another’s. Once you know the best path for you, open a 529 account with at least the minimum required. It could be as little as $5, $25, or in some cases even just $1. Commit to the amount every month. Set up automatic contributions from your checking account, or talk to your employer about payroll deductions. After a few months of these minimum contributions, you may begin to realize that you can afford to increase them. If you can, commit to manageable increases every month until you reach the maximum figure you feel you can contribute. No matter how large or small that amount turns out to be, you will have made a tangible, meaningful difference in the lives of your children and grandchildren.

Start with these three simple steps: Budget, Open, Commit. And when your little loved one decides where they want to expand their educational future, you will have helped them to have a financial head start. Happy New Year and Happy New 529 Account!

About the author: Jørn Earl Otte is Hartford Funds’ Strategic Marketing Consultant for SMART529 in West Virginia.

By Troy Montigney is Vice President of State-Facilitated Retirement Programs (SFRP) at Ascensus

January 3, 2024

Saving for any purpose is a big commitment, worthy of consideration with other long-term goals and any current needs. But even if current needs allow you to make a commitment, doubt can persist, especially when it comes to saving for education in a 529 plan.

The key what-if here, for many, seems to be “what if my loved one doesn’t actually go to college?” Thanks to new federal retirement savings legislation (SECURE 2.0) passed in 2022, another answer to that question takes effect in 2024: move their 529 savings to a Roth IRA.

Congress has a tall task before it to write personal savings policy that aids Americans in navigating many complex choices. But here, it built upon other 529 features like beneficiary changes and usability for trade and apprenticeship programs with the most transformative option yet – in effect, rewarding commitment to save for education with a clear path toward saving for retirement.

While I’d love to focus solely on this new law’s potential, there are some restrictions to keep in mind:

- Time. Your 529 account must be open for at least 15 years before you can make a 529-to-Roth rollover, so saving as early as possible is important. Also, 529 contributions from the last five years, including any associated earnings, are not eligible to be rolled over tax-free. Good things come to those who wait; in this case, you can simply delay the 529-to-Roth rollover to a later year.

- Dollar Limits. 529-to-Roth rollover dollars are subject to annual IRA contribution limits like any regular contribution. There’s also a $35,000 lifetime limit. So in 2024, assuming all other criteria mentioned here are met, you could transfer $7,000 of unused 529 money to a Roth IRA and still have $28,000 of rollover eligibility remaining in future years.

- Ownership. The 529 beneficiary and Roth IRA owner must be the same person, meaning you can’t use your beneficiary’s 529 to fund your own retirement savings. This requires a mindset that the money you’re putting into a 529 is truly for that person, no matter the eventual purpose.

- Income. Already a rule for regular IRA contributions, the Roth IRA owner must have annual earned income equal to or greater than the amount of the 529-to-Roth rollover.

Additionally, treatment of 529s for state income tax purposes can vary from state to state, so it’s important to double-check whether completing a 529-to-Roth rollover will lead to a clawback of any front-end state tax incentives you previously earned for your 529 contributions.

What does this look like in practice? Assuming a 529 beneficiary graduates at age 22 with some money left in her 529, the 529 was opened before she was seven years old, and she moves on to employment with earned income, she could make multiple years’ worth of IRA contributions without straining her budget as a recent college graduate. These early contributions and their decades of potential investment growth would be among the most impactful to her long-term retirement security.

My wife and I are old enough to face many complicated financial decisions year in and year out. (Personally, I’m also still young enough to remember feeling like I was falling behind when my first jobs didn’t offer 401(k)s, and scraping together IRA contributions alongside typical twenty-something expenses was a challenge!) Prioritizing our two young daughters’ 529 plans takes constant commitment, but knowing we could be supporting their retirement, too, is all the reward we need.

About the Author

Troy Montigney is Vice President of State-Facilitated Retirement Programs (SFRP) at Ascensus, which serves over 600,000 IRA savers via CalSavers and Illinois Secure Choice, and nearly seven million 529 accounts in 43 plans across 26 states and the District of Columbia. He previously directed Indiana’s 529 program and lives in suburban Indianapolis with his wife Sara, and daughters Sophie and Molly.